May 22, 2025 • 7 min read

Building trust for low carbon LNG: A joint perspective

The world of energy is transitioning. While the path forward isn’t always straightforward, the shift is unstoppable. Economics, technological innovation and declining environmental capital have set the stage for profound change. We’re working with MiQ, the not-for-profit global leader in methane emissions certification, to deliver that change.

The transition will require a vast amount of new energy infrastructure delivered at unprecedented speed. For this to occur a shift in delivery practices is essential, and trust is at the heart of it1. But instead, trust is declining amidst technological disruption and political uncertainty. Building, maintaining and restoring trust will be fundamental to the energy solutions that succeed in this transition.

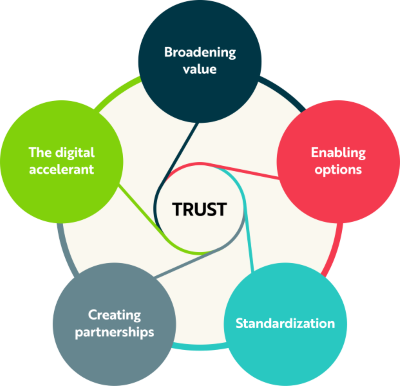

Figure 1 - Trust is fundamental to the five shifts in delivery practice needed to reach the required scale of speed and energy transition infrastructure in the future.1

Liquefied Natural Gas (LNG) is often seen as a key transition fuel but this view isn‘t held universally. Some stakeholders believe LNG offers climate advantages, where others see it as perpetuating outdated fossil pathways.

Recent years have seen the first ‘carbon-neutral’ LNG shipments, involving the offsetting of carbon emissions across the LNG supply chain. While these moves signal demand for lower carbon LNG, they also raise questions around transparency. Initiatives are emerging to address these gaps, but deeper levels of trust are still needed.

Methane and GHG performance certification for LNG can establish that needed trust.

The current state of LNG emissions reporting

Emissions accounting in the LNG and broader oil and gas sectors focus primarily on CO2 and methane. While quantifying both is critical, each presents challenges.

CO2 emissions largely come from continuous plant operations, where flow rates and compositions can be reliably measured and mass balancing methods applied. Methane emissions are often intermittent, arising from start-ups, shutdowns, leaks or malfunctions and are scattered across complex networks such as pipelines and remote equipment, making them harder to quantify.

Table 1 – Comparing CO2 and methane emissions

| Parameter | CO2 emissions | Methane emissions |

|---|---|---|

| Nature of sources | Continuous, from normal plant operations; measurable flows | Intermittent, often linked to non-routine events; hard to predict |

| Measurement approaches | Can be metered, monitored and validated via mass balance | Typically estimated; mass balance often not practical due to small losses over large volumes, and commingled transmission systems |

| Locations (excluding end use) | Industrial facilities, metered fuel use, shipping | Networks of pipelines, remote equipment, numerous potential leak points |

| Importance of fugitives | Low relative to total CO2 rarely a focus | High significance due to methane’s amplified Global Warming Potential (GWP); requires active leak detection and control |

| Reporting practices | High accuracy at facility level (e.g., under EU ETS) | Patchy across supply chains; often relies on estimates or certification |

These differences mean methane accounting must lean on certification frameworks to give stakeholders confidence that emissions are being actively identified and addressed. For CO2, the issue is how emissions are shared between multiple products across the value chain. Without clear and consistent methodologies, product specific carbon intensities can lack comparability and trust. And without tracking along the LNG supply chain, some emissions aren’t assigned to any commercial product, falling between the gaps.

“For benchmarking to be meaningful, we need transparency in not just emissions data, but in how emissions are partitioned across products. Without that clarity, comparisons between facilities or suppliers risk becoming misleading rather than insightful,” says Wrishi Sutradhar, Senior Vice President, Sustainability and Decarbonization Advisory, Worley.

Significant challenges to measurement remain in aligning methodologies to ensure consistent reporting and genuinely comparable emissions data across global LNG markets.

A trust-based LNG approach

The growing push for emissions transparency in LNG is encouraging, but efforts are still fragmented. Without a trusted foundation for emissions claims, buyers and investors struggle to differentiate genuinely low carbon LNG from conventional supply.

This isn't about reinventing the system. A robust framework should build on established, credible standards and methodologies, offering a clear structure to support comparability, verification and informed decision making. We’ve identified three core elements that should be prioritized:

- Standardized methodology for emissions reporting: Consistently applying well-defined scopes, boundaries and emission factors across the LNG value chain, aligning where possible with frameworks like OGMP 2.0, the Greenhouse Gas (GHG) Protocol or national MRV systems. Wide variation in how carbon intensity is defined, measured and reported compromises meaningful comparisons.

- Independent validation: Certification programs and third-party assessments play a critical role in enhancing stakeholder confidence. Third-party audits allow unbiased assessments. These audits provide performance results against the standard that can help to build trust and market assurance.

- Clear benchmarks and context: Beyond raw data, stakeholders need clarity on what the numbers mean: intensity thresholds, regional and global averages and guidance on interpreting uncertainty. From Ambition to Reality 4 (FATR4), the latest in our collaborative series with Princeton University, focuses on new methods for project delivery to meet the unprecedented infrastructure challenge. The paper concluded that trust isn’t just about numbers, but how information is communicated, understood and used.

Credible frameworks for supporting low emission global LNG transactions, like the MiQ Certificate Inter-Regional Import System (CIRIS), can provide support in this area, building trust and assurance with traders and regulators with minimal disruptions to existing trading practices. The real challenge lies in integrating and iterating them, encouraging diverse stakeholders to work from common reference points.

An independent, practical approach

A certified gas market based on methane emissions performance could play a significant role in achieving efficient, cost-effective emission reductions for the oil and gas sector. For this to work, the market must be credible to participants, NGOs, and regulators. Once trust and transparency are achieved, the market has the potential to take off on a global scale.

With 2030 emission reduction targets looming and a changing policy landscape, we don’t have time for climate regulations to be put in place to drive down emissions. The voluntary methane performance certification market represents the best bet for emission reductions at scale. It’s in our interest that the market is set up according to concrete principles. Trying to address issues after projects start will be too late, and market, regulator and public confidence will be lost.

Given the development of the certified gas space, basic principles establishing transparency and trust will be needed for all programs participating in this. As we’ve seen with attempts at market developments in other sectors, the risk of greenwashing is real. Not taking greenwashing seriously can result in the certified gas market being undercut and result in market collapse – and therefore resulting in the collapse of one of the most cost-effective ways to drive down methane emissions from the oil and gas sector.

“A transparent certified methane performance gas market is possible through the application of principles, like those established by MiQ, that build the credibility of the certified gas market,” says Ben Webster, Director of Policy, MIQ.

Incorporation of these principles will allow it to function efficiently and build trust amongst market participants. The principles should be structured into the certification element of an environmental attribute market – including the methane performance space. MiQ identifies four key principles:

- Principle 1: Transparent, robust standards

- Principle 2: Third-party audits

- Principle 3: Facility-wide certification

- Principle 4: Marketable

“For methane certification to have maximum impact, the market needs robust, defensible standards and a credible and transparent foundation. Changing or abandoning market rules and principles down the track will only lead to continued emissions releases and an ineffective market,” says Webster. Certifiers, producers, buyers and other stakeholders need to see these principles as essential to the certified gas market's energy transition potential.

“MiQ’s methane performance certificates and CIRIS offer a transparent and verifiable system that facilitates both emissions reductions and efficient LNG transactions”, says Webster. In combination with its digital registry, the MiQ framework can be used for coupled (bundled) and decoupled (unbundled) transactions of methane performance certificates. This flexibility allows traders and businesses to buy and sell the certificates or the gas in different ways depending on their needs.

The MiQ standard was built to complement the existing global gas and LNG trading market, allowing for rapid market adoption. Though already accepted in the energy space, we need broader adoption to incorporate these principles into certification, tracking and transactions, providing the credibility the market needs and assurance for parties and stakeholders. Common reference points like these build trust and credibility elements, which lie at the heart of any global methane performance-certified gas (and LNG) market.

Next steps for LNG

The LNG sector has made meaningful progress in emissions transparency, but fully delivering on this promise will take broader alignment, more transparent disclosures and the courage to act, even with imperfect data. Buyers, investors and regulators want greenhouse gas intensity data they can trust. The challenge is how quickly we can scale consistent reporting and verification practices across diverse regulatory and commercial landscapes.

The next phase should focus on building on existing frameworks like OGMP 2.0, the MiQ’s CIRIS framework and Supply Chain Protocol, and national or regional MRV systems, not creating new, untested ones. The priority is adoption, convergence and disclosure. This will help improve comparability over time, giving buyers confidence to make more sustainable and efficient choices.

A coordinated approach leveraging both certification and digital tracking could help close the gap between upstream, midstream and delivery-related emissions. This gives us an opportunity to shift from pilot initiatives to a system-wide model of trust that fosters collaboration.

“We’re not looking for perfection, but transparency, accountability and constant improvement,” says Sutradhar.

1 “From Ambition to Reality”, (2021, 2022, 2023 and 2024), by Worley and Princeton University’s Andlinger Center for Energy and the Environment. Available at https://www.worley.com/en/insights/our-thinking/energy-transition/from-ambition-to-reality

Contributing authors

- Ben Webster, Director of Policy, MIQ

- Wrishi Sutradhar, Senior Vice President, Sustainability & Decarbonization Advisory, Worley

- Ian Moore, Technical Director, EMEA Low Carbon, Worley Consulting

- Paul Ebert, Group Director – Sustainability & Energy Transition Leadership, Worley